This website, owned by Alantra Partners S.A., uses cookies, including third-party cookies, to better understand how you use our website, offer better functionality and customization levels. For more information on how we use cookies, please see our Cookie Policy. Please, configure your cookie preferences or accept them all to continue navigating in our website.

These are the cookies we use on our website. You can configure your preferences and choose how you want your data to be used for the following purposes.

Own / Mandatory / Technical

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences or filling in forms.

Analytical cookies:

These cookies collect information regarding the use of the web page, such as time spent on the page and content visited, to measure its performance and improve navigation.

Notes from EQMC – Rich pickings in pan-European small-caps

Notes from EQMC – Rich pickings in pan-European small-caps

In our second Notes from EQMC, we highlight the factors which underpin the structural opportunity in European small-caps and what makes the risk/reward look attractive. EQMC targets high-quality companies within this space and uses an active engagement toolkit to further enhance value creation.

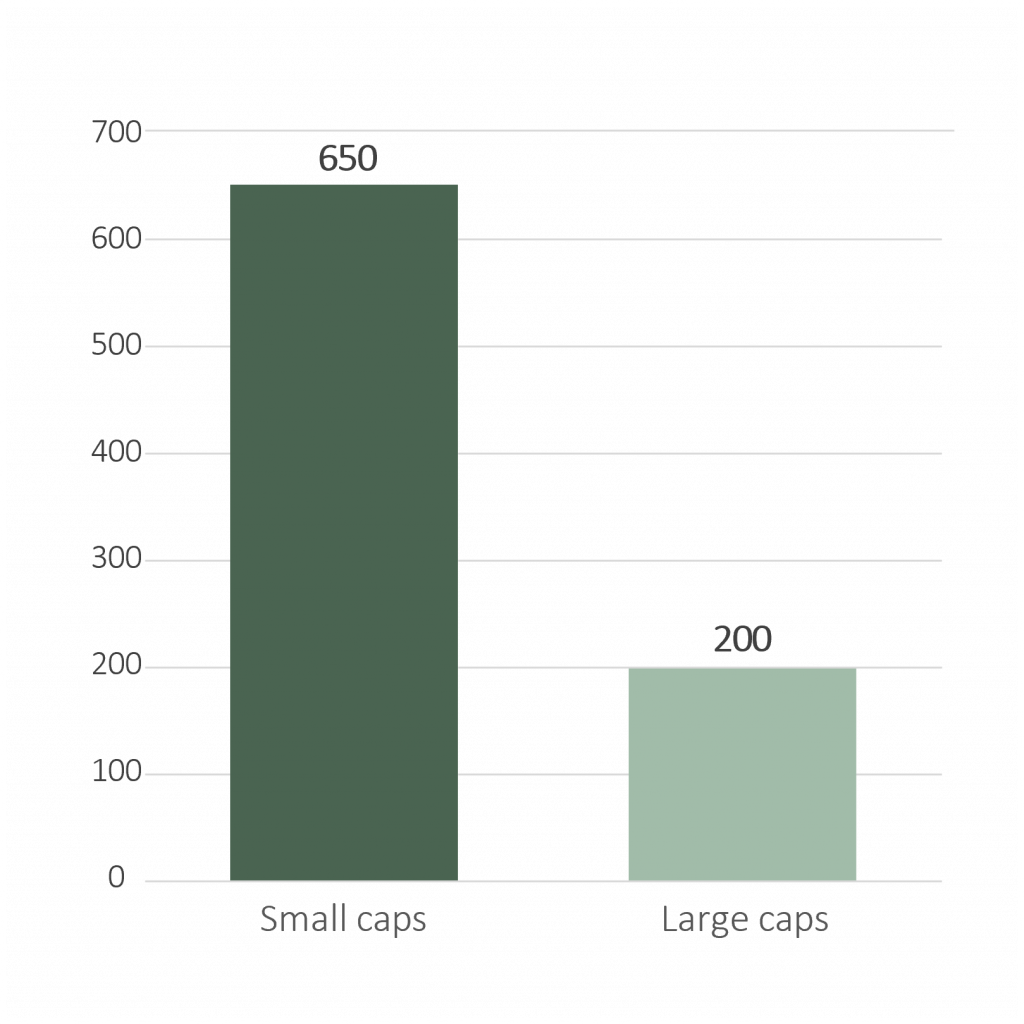

Taking a pan-European approach to small caps has several advantages. First, there is the higher growth potential that small caps have over large caps, with almost 4x the number of companies with return on capital employed (ROCE) >20% (as illustrated below). As EQMC’s process looks to identify quality companies, ROCE is a key metric for evaluating solid investments and avoiding value traps.

# of high-quality companies (ROCE>20%)*

(*) Source: ROCE calculated as EBIT/Capital Employed. Based on Bloomberg data

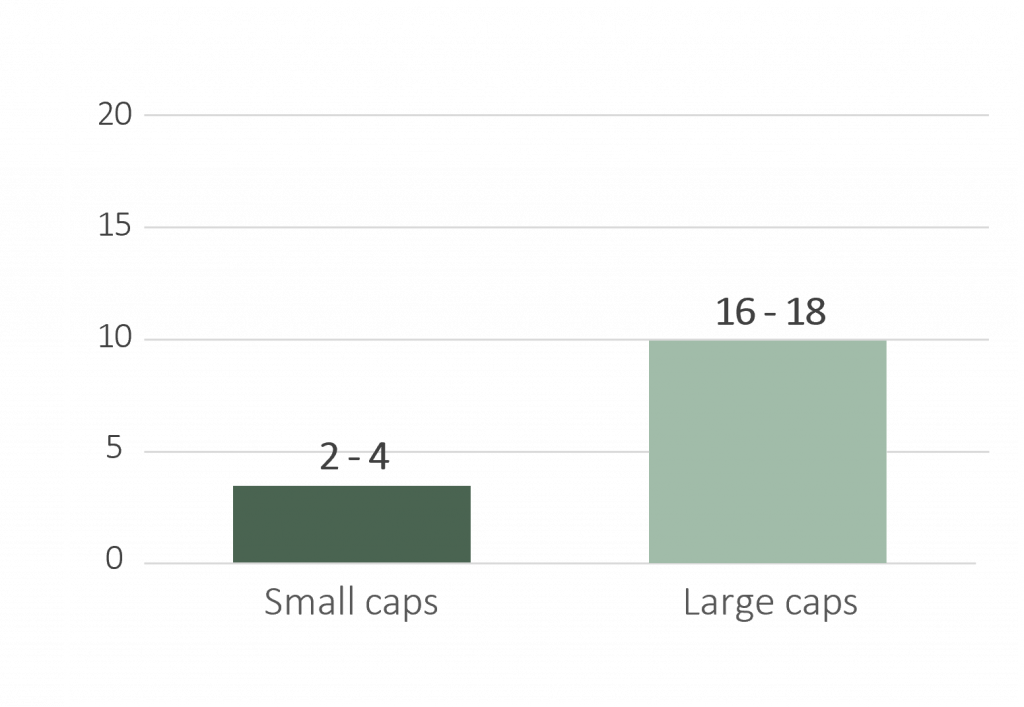

Second, the low level of analyst coverage in this market results in mispricing opportunities. As a function of MIFID II regulation and the unbundling of commissions, brokerage houses have drastically reduced their coverage of the small-cap market. The average stock is covered by just two to four Analysts versus 16 to 18 in the large-cap space.

Analyst coverage per company*

(*) Average number of analysts covering a company taking a random sample high quality companies both in Small Caps (100 out of 400) and Large Caps (50 out of 105)

Third, is choice. There are more than 2,000 companies with a market cap below €2bn in EQMC´s target sectors. After our filtering process, this translates to a manageable 60 to 80 stocks being covered per EQMC Analyst. EQMC has a proprietary process and one of the most prominent teams in the European small cap space, with over 15 investment professionals who combine vertical and geographical expertise.

Fourth, this is a market where active engagement makes a difference. Companies of this size tend to not be overbanked or overrun by management consultants. Leaders of these firms are often first-time CEOs, who are typically more open to a constructive significant shareholder seeking to engage, drive operational excellence and look for transformational changes to unlock significant unrealised value.

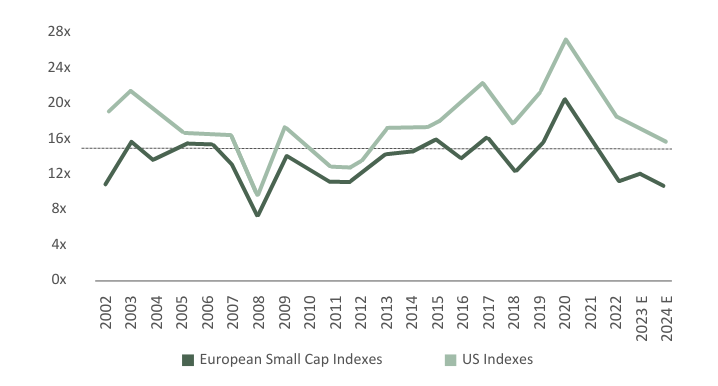

Finally, on valuation, European small-caps currently offer a significant valuation discount over historical levels (as illustrated below), trading at 12x P/E 2023, well below the 15x long-term levels seen previously. This dislocation is particularly relevant in the UK (with political uncertainty impacting the market) and Germany (with gas supply concerns ongoing despite recent modest de-risking). In both the UK and Germany, markets are trading at 9-11x P/E, having historically traded at the upper range of c.14-15x.

European small caps1 trading at c.25% discount to historical levels

Notes: 1) Small Cap EU indexes includes average of German SDAX, CAC Small Cap, FTSE Small Cap, Switzerland Small Cap, Ibex Small Cap, Italy Small Cap, Sweden Small Cap, Norway Small Cap, Euro Stoxx Small Cap, Russel Europe Small Cap, FTSE Develop European Small Cap; 2) US indexes include Dow Jones and S&P 500; 3) UK: PE multiple from the FTSE Small Cap, Spain: PE multiple from Ibex Small Cap, Norway: PE multiple from Norway Small Cap; Germany: PE multiple from SDAX, Sweden: PE multiple from Sweden Small Cap

Against this backdrop, the potential for growth in small-cap companies needs to be considered. These companies are often overlooked by larger institutional investors, which reduces competition and increases the potential for mispriced assets. Smaller companies are often more nimble and able to pivot faster than larger companies, making them more responsive to changes in the market. They also tend to specialise in niche markets, allowing them to become experts in their field and gain a competitive advantage.

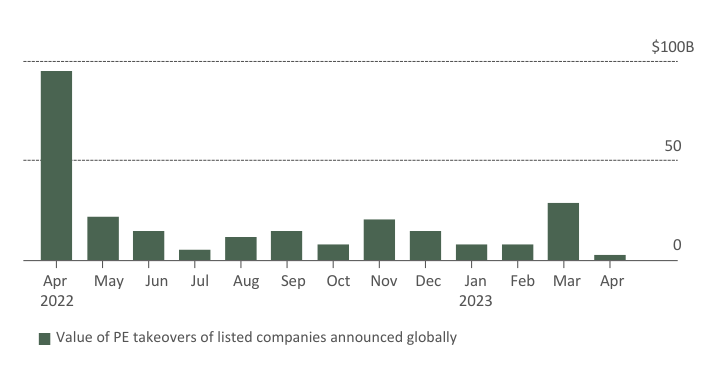

As we begin to see M&A activity pick-up (as illustrated below), we believe part of this uptick will be in the form of US to European deal activity. Inflation and geopolitical risks are stabilizing, which is improving buyer confidence and could be a spur in interest in European targets, particularly given the low valuations and the relative strength of the dollar.

Private Equity Buyout Deals Bounced Back in March

Source: Bloomberg

Since EQMC’s inception in 2010, the structural opportunity in European small caps has expanded given MIFID regulation and other factors affecting sell-side coverage. Over this time, our process has evolved to filter and source the right opportunities from a deep pool of under-researched quality companies where our engagement can add value. With the added tailwind of a dislocation in valuations, the opportunity in this market shows little sign of slowing.