Macro Update – May 2024

Macro Update – May 2024

Despite recent fluctuations, the forecast for the year remains stable, with expectations of solid global growth and gradual disinflation. In the US, a predicted moderation in demand growth due to higher long-term interest rates should help manage inflation effectively. The Eurozone is outperforming expectations, while China is implementing necessary measures to achieve approximately 5% growth. Japan may reduce its public debt purchases to better support the yen. The outlook for equities is positive, particularly in Europe and emerging markets, although risks such as inflation and fiscal credibility persist. This situation prompts a cautious approach to long-term bonds.

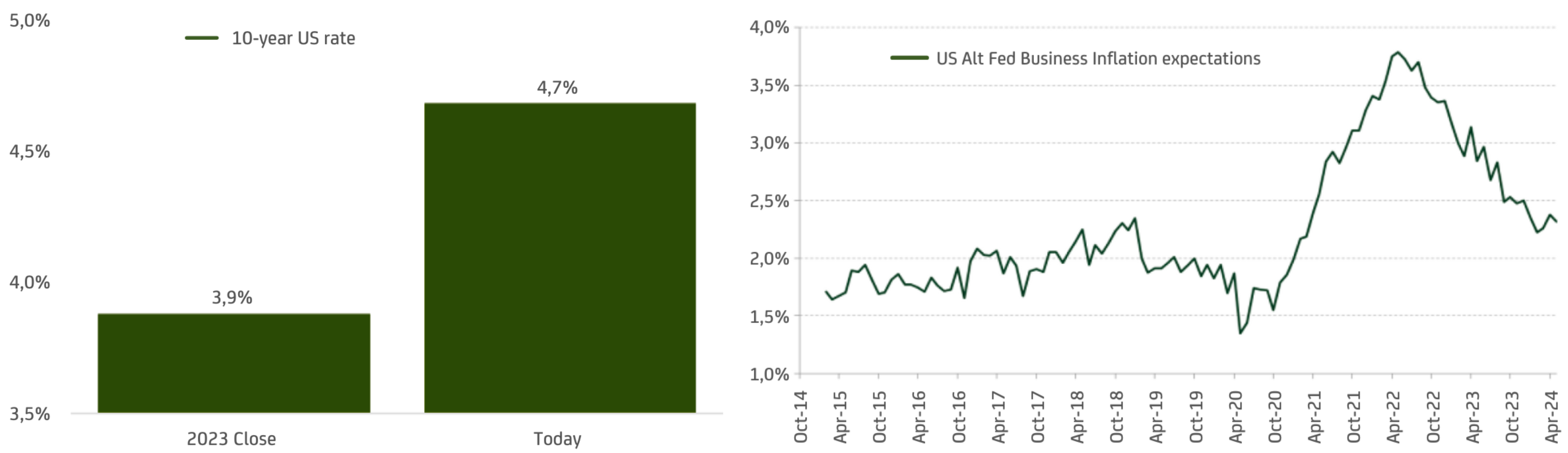

Recent spikes in American inflation are concerning; however, the US is expected to continue its disinflation trend from the latter half of the last fiscal year. This outlook is supported by: An increase in long-term rates since the year’s start; suggesting tighter financial conditions; a predicted moderation in aggregate demand; a stable inflation expectation; recent signs of decreasing wage growth and labour market statistics, such as declining job vacancies and quit rates, which indicate a rebalancing of supply and demand.

The likelihood of stagflation is low, bolstered by well-anchored inflation expectations. Meanwhile, signs that the labour market is rebalancing suggest that the Federal Reserve’s policies might be sufficiently restrictive to achieve the 2% inflation target. Nonetheless, the resilience of US aggregate demand suggests a higher neutral interest rate than pre-pandemic, which leads to expectations of few rate cuts in the current cycle.

Economic Activity in the Eurozone: The region is gradually improving, with anticipated growth of around or above 1% in 2024. This positive trend is supported by: Rising real wages, low unemployment rates, healthy household finances, potential benefits from the resolution of inventory adjustments and supportive fiscal policy and low long-term real interest rates.

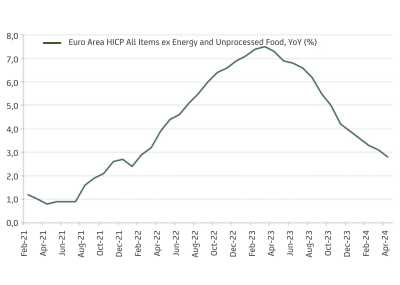

Core Inflation Trends in the Euro area: Core inflation is moving in the right direction, which is promising given that inflation expectations remain well-anchored.

ECB Policy Outlook: The European Central Bank appears dovish and has virtually guaranteed a rate cut in June, influenced by economic challenges in Germany and poor fiscal data from countries like France. However, with expected economic acceleration in the eurozone over the year, interest rates in our region may fall less than currently anticipated by the ECB.

Our Global Economic Outlook for 2024:

China: Anticipated growth rates around 5%, driven by increased stimulus and potential stabilization in the property sector in the second half of the year.

Emerging Asia excluding China: High average growth is expected, supported by a strong commitment to macroeconomic stability through credible fiscal and monetary policies.

Latin America: Despite concerns about the economic policy direction in several countries, a positive economic performance is expected, particularly in countries such as Mexico and Brazil.

Japan: With wages rising above inflation, private consumption is expected to boost GDP growth to exceed potential this year. The Bank of Japan may further normalize its monetary policy by reducing public debt purchases before next August, potentially stabilizing the yen.

Equity:

The macroeconomic outlook supports a constructive stance on equities, advising a balanced mix between value and growth styles, with a preference for European over US equities due to better growth prospects and valuations. Emerging Asian equities, including China, are recommended for their potential economic improvement and attractive valuations.

Government Bonds:

Caution is advised for longer US yield segments due to fiscal risks and potential inflation surprises. German bonds appear overvalued given the strengthening eurozone economy, while long-term Japanese yields might rise soon, influenced by potential changes in BOJ policies.

Corporate Bonds:

Preferred due to healthy balance sheets and low default risks, especially when combined with emerging market local currency debt in well-governed markets with stable economic conditions.

Currencies:

The ECB’s dovish stance could weaken the euro, making currencies like the NOK, NZD, AUD, and GBP attractive in developed markets. In emerging markets, currencies from countries with strong governance and high growth prospects are favoured. The dollar is seen as slightly overvalued and only moderately preferred due to fiscal concerns and a shrinking growth differential with Europe in 2024.

This report has been prepared by AMCHOR Investment Strategies SGIIC, S.A. (“AMCHOR IS”) an entity participated by the Alantra Group and incorporated as an investment firm authorized and supervised by the CNMV, registration number 273 with registered office at Calle Velázquez Nº 166, 28002 Madrid (Spain).

This report is addressed only to professional investors for internal and exclusive use. The information contained herein shall only be distributed as permitted by applicable law and AMCHOR IS and the Alantra Group specifically forbid the redistribution of this document in whole or in part without its prior written permission.

Nothing in this report constitutes a representation from AMCHOR IS or the Alantra Group that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. This report is published solely for information purposes, it does not constitute an advertisement and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments in any jurisdiction. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor it is intended to be a complete statement or summary of the securities or financial markets referred to in this report.

AMCHOR IS and the Alantra Group do not (i) endorse, guarantee nor represent that investors will obtain profits nor (ii) accept any liability for any investment that the recipients may carry out and incur in losses arising from adopting the recommendations included in this report or its contents. Investments involve risks and investors should exercise prudence in making their investment decisions. This information has been extracted from public sources that AMCHOR IS considers reliable and is not responsible for its truthfulness or accuracy. This report should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this report are subject to change. The analysis contained herein is based on numerous assumptions, hypothesis and forecasts. Different assumptions could result in materially different results. AMCHOR IS and the Alantra Group are under no obligation or keep current the information contained in this report.

The investor should note that the financial market is fluctuating and as such is subject to variations. The price of investments (which may be quoted in illiquid markets) may change and the investor may not get back the amount initially invested. The figures contained herein relate to the past. Past performance is not a reliable indicator of future results.