Macro Update – July 2025

Macro Update – July 2025

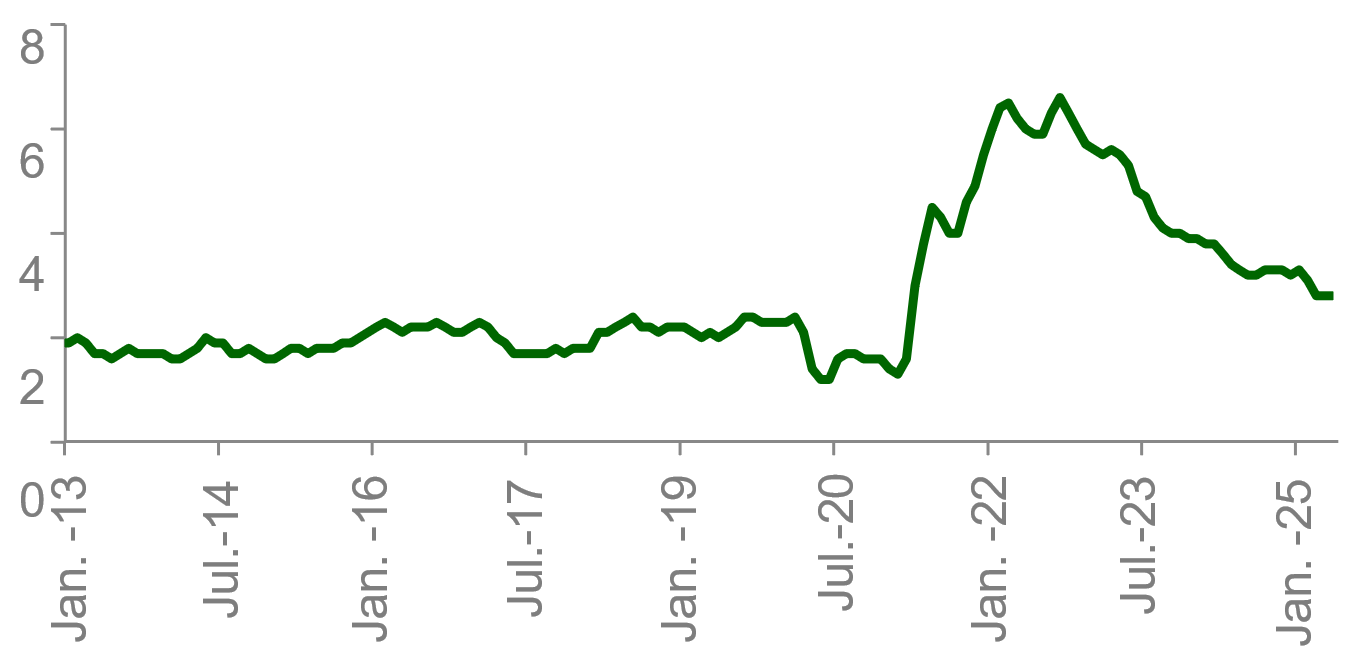

In the United States, inflation is expected to rise significantly in the coming months due to higher tariffs and the sharp depreciation of the dollar since the beginning of the year. Nevertheless, the risk of a recession remains low, supported by strong household and corporate balance sheets.

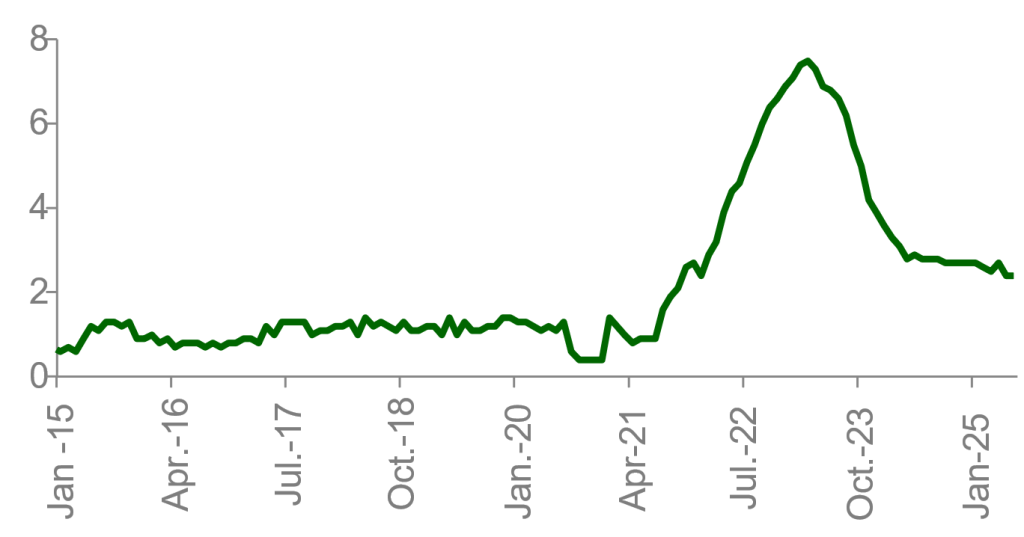

In the Eurozone, the euro’s strong appreciation is likely to push inflation below 2%, giving the European Central Bank (ECB) more flexibility to ease policy if needed. Germany’s planned fiscal stimulus should support growth, though political uncertainty in France and the negative impact of a strong euro on exports remain key risks.

The United Kingdom is facing growing fiscal credibility concerns after the Labour-led government failed to deliver on previously announced spending cuts. Meanwhile, Asia ex-Japan continues to stand out for its solid growth prospects and macroeconomic stability, with moderate inflation and balanced external accounts. Japan could see modest rate hikes if wage growth gains traction, although structural headwinds suggest rates will remain low overall.

Against this backdrop, a cautious approach to equities is warranted, favoring Europe and Asia over the U.S. alongside selective exposure to fixed income in countries with declining inflation and sound fiscal fundamentals.

United States

Inflation is likely to rise in the coming months due to higher tariffs and the dollar’s depreciation. We remain concerned about the country’s weak fiscal position, especially following Trump’s new fiscal package and his pressure on the Federal Reserve. Still, as long as tariff hikes remain moderate and the term premium is contained, the risk of recession remains low.

U.S. Core Inflation

The Eurozone

The strong appreciation of the euro could drive headline inflation clearly below 2% for the remainder of the year, providing the ECB with greater flexibility to lower interest rates if any signs of economic weakness emerge. Additionally, Germany’s government is moving quickly to approve fiscal stimulus measures, which should help generate a cyclical rebound in the second half of the year. On the risk side, we must closely monitor the political situation in France and the potential negative effects of a strong euro, and higher tariffs, on European exports.

Eurozone Core Inflation

China & emerging Asia

We see very solid growth, especially in relative terms. In 2025, it is likely that emerging Asia will grow at a 4-5% pace, compared to the 1-1.5% expected for the U.S. The region shows enviable macroeconomic stability, with moderate and declining inflation, credible central banks, broadly balanced external accounts, and sustainable fiscal deficits and public debt levels.

Even China, which was expected to be the country most affected by tariffs, has left behind the most catastrophic scenarios and has managed to sustain annual growth rates slightly above 5% in the first half of the year through stimulus measures.

Japan

As long as wages show sufficient strength and the tariff situation remains under control, it is reasonable to expect aggregate demand growth slightly above potential, leading to a sustainable stabilization of inflation around 2%. In that scenario, another rate hike by the BOJ later this year would be very likely. However, we do not expect the terminal rate to be particularly high in this cycle, because even with near-zero nominal rates and an expansionary fiscal policy, Japan’s economy is still struggling to overheat, clearly indicating that the neutral rate in the country is quite low.

Market Outlook & Asset Allocation

Equities

Tight valuations and the presence of significant risks lead us to adopt a slightly more cautious stance on equities. In terms of geographic diversification, we continue to recommend underweighting the U.S. and overweighting both Europe and, especially, Asia ex-Japan, as we see lower tariff-related risks and particularly favourable relative growth prospects.

Government Bonds

The recent drop in long-term yields leads us to prefer a more moderate duration stance. Relatively speaking, we continue to favour the 10-year segment in countries with declining inflation and reasonably strong fiscal positions.

Credit

We continue to favour greater exposure to Investment Grade over High Yield and generally prefer shorter maturities.

Currencies

Although we do not rule out some short-term appreciation if the market begins to price in a more hawkish Fed response to rising U.S. inflation over the summer, we remain negative on the dollar due to the country’s challenging fiscal outlook and political pressures on the Fed’s independence. We are cautious on the yen, given its low carry and Japan’s high public debt levels.

This report has been prepared by AMCHOR Investment Strategies SGIIC, S.A. (“AMCHOR IS”) an entity participated by the Alantra Group and incorporated as an investment firm authorized and supervised by the CNMV, registration number 273 with registered office at Calle Velázquez Nº 166, 28002 Madrid (Spain).

This report is addressed only to professional investors for internal and exclusive use. The information contained herein shall only be distributed as permitted by applicable law and AMCHOR IS and the Alantra Group specifically forbid the redistribution of this document in whole or in part without its prior written permission.

Nothing in this report constitutes a representation from AMCHOR IS or the Alantra Group that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. This report is published solely for information purposes, it does not constitute an advertisement and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments in any jurisdiction. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor it is intended to be a complete statement or summary of the securities or financial markets referred to in this report.

AMCHOR IS and the Alantra Group do not (i) endorse, guarantee nor represent that investors will obtain profits nor (ii) accept any liability for any investment that the recipients may carry out and incur in losses arising from adopting the recommendations included in this report or its contents. Investments involve risks and investors should exercise prudence in making their investment decisions. This information has been extracted from public sources that AMCHOR IS considers reliable and is not responsible for its truthfulness or accuracy. This report should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this report are subject to change. The analysis contained herein is based on numerous assumptions, hypothesis and forecasts. Different assumptions could result in materially different results. AMCHOR IS and the Alantra Group are under no obligation or keep current the information contained in this report.

The investor should note that the financial market is fluctuating and as such is subject to variations. The price of investments (which may be quoted in illiquid markets) may change and the investor may not get back the amount initially invested. The figures contained herein relate to the past. Past performance is not a reliable indicator of future results.