Macro Update – January 2024

Macro Update – January 2024

Given the recent significant easing of financial conditions, if this trend persists, our 2024 economic growth forecasts may need upward revisions. In the U.S., we could now expect expansion rates surpassing 2%, and in the Eurozone, there might be a notable acceleration with growth rates well above 1%. While short-term underlying inflation is anticipated to decline, a potential stronger aggregate demand due to relaxed financial conditions could introduce certain upside risks throughout the year.

Beyond Europe and the U.S., our 2024 macroeconomic scenario remains unchanged, with promising performance in emerging economies (including approximately 5% growth in China). The Bank of Japan is expected to take gradual steps towards monetary policy normalization, contingent on a robust wage dynamic.

Market positioning recommendations include prudent yet constructive equity positions (especially in Europe and emerging markets, favoring cyclical/value positions), a reasonably positive outlook for credit and emerging market local currency debt, and a cautious stance on duration, with a clear preference for short segments of yield curves.

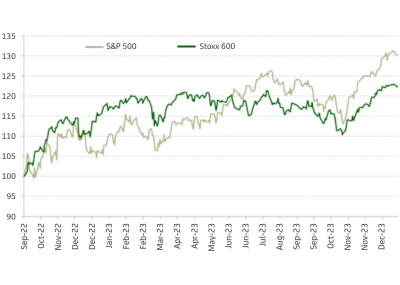

During the latter part of 2023, we have witnessed a very significant relaxation of financial conditions globally. Long-term government bond yields have fallen appreciably, credit spreads have continued to tighten and we have also observed a very bullish performance in equity markets.

In both the US and the Eurozone, robust fundamentals support aggregate demand (healthy household and corporate balance sheets, growing real wages, low unemployment levels ensuring job security and consumer enthusiasm, no significant supply excesses limiting downside risk in corporate investment, expected end of downward adjustment in industrial inventories boosting activity, and strong public spending on ecological transition and defense).

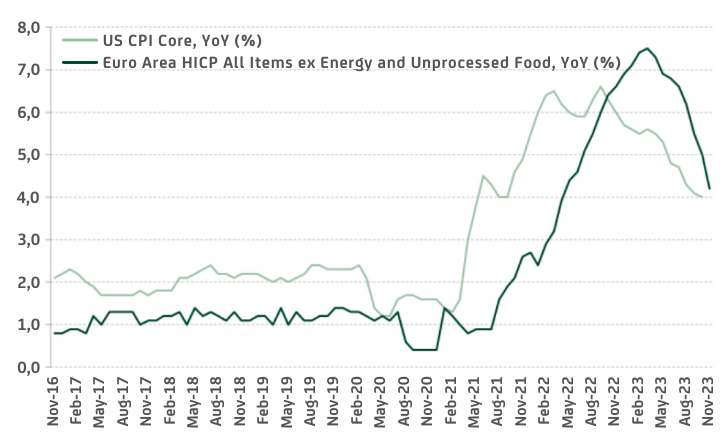

In this context of strong demand and a likely positive output gap, excessively relaxed and persistent financial conditions could endanger the ongoing deflationary process in most developed economies.

Considering the aforementioned factors, it is likely that the interest rate cuts in 2024 by central banks will be less ambitious than currently expected. Simultaneously, a lower degree of monetary activism may coincide with upward revisions of neutral rate estimates, both short and long term.

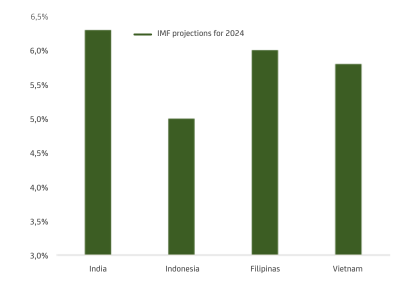

The macroeconomic outlook for emerging economies in 2024 remains reasonably positive, especially in Asia and some Latin-American economies. These regions exhibit solid economic growth rates, controlled inflation, lower deficit and public debt levels than developed countries, and central banks that have been able to proove their anti-inflationary credibility.

Even in China, where uncertainties may very well persist, we anticipate growth rates of around 5% this year. The adjustment in the real estate is ongoing but it is clearly more advanced than 12-24 months ago; authorities lean towards introducing monetary and fiscal stimuli, and the industrial inventory adjustment is likely concluding. As memories of the pandemic fade, consumer sentiment should also improve.

In contrast, Japan may take further steps towards monetary normalization, likely by April, contingent on confirming a dynamic wage evolution. With growth exceeding potential, a positive output gap, sustained upward movement in household and business price expectations, and a prolonged period of underlying inflation above the 2% target, the conditions seem to be coming into place for the BOJ to be able to raise rates a little bit and further ease its yield curve control policy.

Fixed Government Income:

Following significant declines in long-term interest rates in both the United States and Europe, we approach duration risk with caution, preferring to focus on short segments of the yield curves. In Japan, we forecast a significant rise in the 10-year bond yield within a 3-6 month horizon.

Equity:

Perceiving macroeconomic conditions in the U.S. and Europe avoiding recession, and expecting structurally elevated real interest rates, we maintain the belief that the cyclical market segment, including European banks, should outperform the defensive one. Geographically, given the mentioned factors and relative valuations, we favor European and Asian markets over North America.

Credit:

We still favor corporate fixed income, anticipating reasonably stable default rates in our central macroeconomic scenario. At the same time, and because spreads aren’t high, combining credit exposure with well-selected positions in emerging market local currency debt makes sense. This latter asset class appeals to us due to promising return prospects, potential currency appreciation, in a context in which see several emerging countries with relatively high expected growth rates, solid economic governance, low public deficits, and controlled inflation—factors that reduce the perceived risk of exposure to local currency debt.

Currencies:

We anticipate a narrowing growth differential between the U.S. and Europe in 2024, so it is not impossible that the euro could do well against the dollar this year. We hold a positive view on currencies like NOK, NZD, or AUD, and still favor currencies of emerging countries with strong macroeconomic governance and favorable growth prospects (BRL, INR, MXN, IDR, for example). Considering positive macro signals from Japan, we see the yen (in prudent doses) as a potentially good protective position in the coming months.

This report has been prepared by AMCHOR Investment Strategies SGIIC, S.A. (“AMCHOR IS”) an entity participated by the Alantra Group and incorporated as an investment firm authorized and supervised by the CNMV, registration number 273 with registered office at Calle Velázquez Nº 166, 28002 Madrid (Spain).

This report is addressed only to professional investors for internal and exclusive use. The information contained herein shall only be distributed as permitted by applicable law and AMCHOR IS and the Alantra Group specifically forbid the redistribution of this document in whole or in part without its prior written permission.

Nothing in this report constitutes a representation from AMCHOR IS or the Alantra Group that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. This report is published solely for information purposes, it does not constitute an advertisement and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments in any jurisdiction. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor it is intended to be a complete statement or summary of the securities or financial markets referred to in this report.

AMCHOR IS and the Alantra Group do not (i) endorse, guarantee nor represent that investors will obtain profits nor (ii) accept any liability for any investment that the recipients may carry out and incur in losses arising from adopting the recommendations included in this report or its contents. Investments involve risks and investors should exercise prudence in making their investment decisions. This information has been extracted from public sources that AMCHOR IS considers reliable and is not responsible for its truthfulness or accuracy. This report should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this report are subject to change. The analysis contained herein is based on numerous assumptions, hypothesis and forecasts. Different assumptions could result in materially different results. AMCHOR IS and the Alantra Group are under no obligation or keep current the information contained in this report.

The investor should note that the financial market is fluctuating and as such is subject to variations. The price of investments (which may be quoted in illiquid markets) may change and the investor may not get back the amount initially invested. The figures contained herein relate to the past. Past performance is not a reliable indicator of future results.